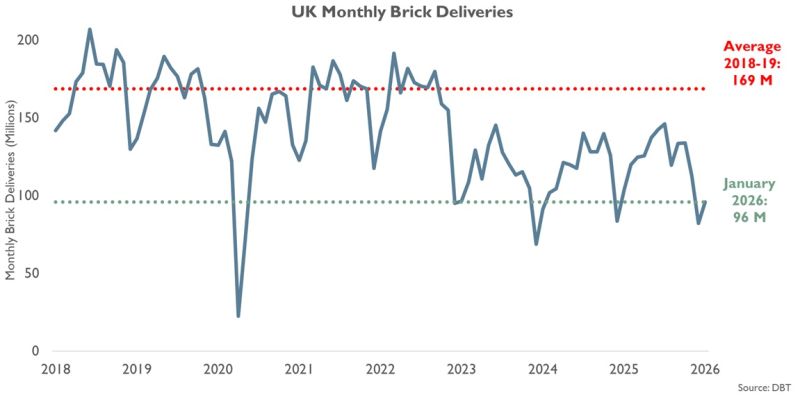

UK brick deliveries fell at the start of 2026, adding to doubts over whether housebuilding activity will rebound strongly this year after a weak 2025. Deliveries in January were 7.6 per cent lower than a year earlier, according to Department for Business and Trade data, in a closely watched indicator for new housing starts at a time when monthly starts figures are not available.

The decline, however, comes with caveats. January activity was affected by persistent rain, while the comparison was against a relatively strong month a year earlier, when housebuilding was still recovering before activity tailed off from April 2025.

That has left the sector with only limited evidence so far that demand has picked up in the way some commentators had expected. After uncertainty around the Autumn Budget weighed on demand in the third and fourth quarters of 2025, some had predicted a rush of housing demand in the opening months of this year. So far, there is little sign of that, although it remains early in 2026.

The underlying pressures facing housebuilders also appear little changed from last year. In higher-value parts of the market, affordability and buyer demand remain the main constraints. In more affordable areas, the bigger problem is site viability, with developers continuing to weigh build costs against achievable sales values.

Other structural issues have also persisted into this year. High-rise development is still being slowed by delays at the Building Safety Regulator’s Gateway 2 and 3 stages, while housing associations are still not buying Section 106 affordable units, removing an important outlet for some schemes.

For the industry, the next major test will be the spring selling season, which is typically one of the most important periods of the year for housebuilders. That matters all the more because demand fell away sharply in that period last year, making the coming months a more meaningful guide to how 2026 may unfold.

Fresh risks have also emerged. The recent rise in conflict in the Middle East threatens to further weaken already subdued consumer and homebuyer confidence, while also pushing up input costs for builders. Construction product prices in January were already 41.6 per cent higher than in January 2020.

Supply disruption is expected to be limited because around three-quarters of construction products used in the UK are made domestically. But higher energy prices are likely to increase manufacturing costs, particularly for energy-intensive producers, where energy can account for up to a third of total costs. Stocks and partial hedging may delay the impact, but unless the conflict eases quickly, further price rises look likely.

The wider concern is that greater geopolitical uncertainty will feed through into higher inflation and reduce the scope for interest rate cuts, keeping mortgage costs higher for longer.

At the start of the year, many housebuilders and developers expected starts to rise by a high single-digit percentage from a very low base in 2026, with completions up by a low single-digit percentage. That outlook has not disappeared, but it is now overshadowed by greater uncertainty and a growing list of downside risks.