Intelligence

INTELLIGENCE: Float glass inflation widens pressure on glazing firms as supply tightens

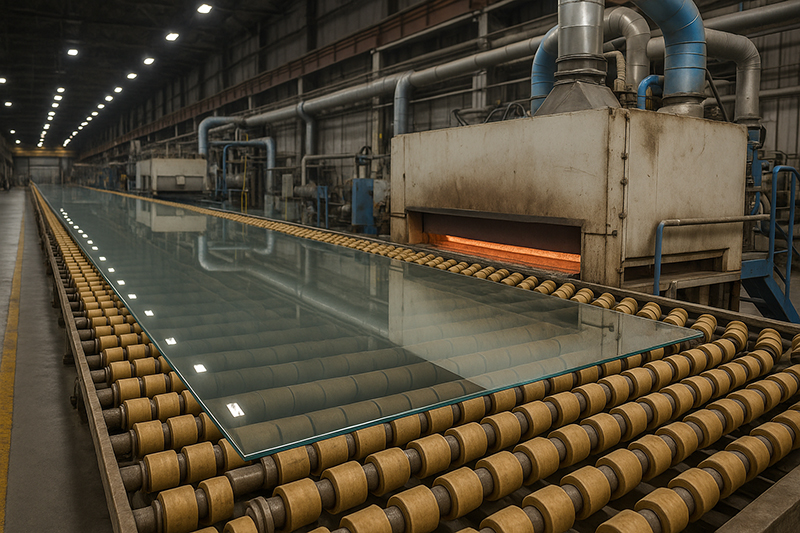

Rising float glass prices are imposing fresh strain across global glazing supply chains, forcing manufacturers and installers to reassess margins, sourcing decisions and contract structures. New data from IMARC Group shows UK spot prices reached about US$863 per tonne in the second quarter of 2025, up from roughly US$820 in the first. Germany and France posted second-quarter prices of US$637 and US$664 per tonne, pointing to broad firmness across Western Europe.

These increases are now filtering through to insulated glass unit producers, window and curtain-wall manufacturers and installation businesses, many of which are finding it tougher to absorb higher costs. Energy remains the key pressure point. Float-glass production depends on furnace operations that require continuous high-temperature firing, and with electricity and natural-gas charges still well above historical norms in Europe, operating budgets have grown heavier month by month. Raw-material costs for soda ash, silica sand and dolomite have also climbed, while transport issues and maintenance backlogs have narrowed supply further.

Several glass-melting plants in Western Europe have announced scheduled shutdowns for furnace maintenance or reductions in output to contain expenses. These measures have tightened availability enough to give producers more control over pricing even though downstream demand is steady rather than buoyant. In the UK, where domestic supply is already limited, the combined effects of higher energy charges and furnace downtime have magnified the pressure on buyers.

For British glazing manufacturers and installers, the implications are considerable. Margins risk shrinking unless higher procurement costs can be shared with fabricators or end clients. Fixed-price obligations agreed before the latest round of inflation may be difficult to honour. Concerns over delivery times are growing as suppliers warn of slower turnaround during maintenance periods, posing challenges for large commercial projects and public-sector refurbishments. Some companies have begun building cost-indexing mechanisms into their purchasing arrangements, while installation firms are adding price-adjustment clauses to future bids to guard against further volatility. Others are assessing overseas sources, although freight costs, tariff exposure and compliance with European specifications remain obstacles.

The situation is not uniform across regions. In Asia, pressures are milder: South Korea reported second-quarter prices near US$421 per tonne, a sharp contrast to Europe. That gap is prompting more buyers to consider longer supply routes, though the financial and logistical trade-offs remain significant.

Looking ahead, IMARC expects continued firmness in markets where capacity is tight and energy charges remain high. For the glazing trade, this suggests a period in which procurement plans, contract terms and stock policies may need closer scrutiny to manage ongoing cost strain in the float-glass segment.

Why This Matters: Putting a actual value on the price rises focuses the mind of the significance of the cost pressures in the market. This information needs be passed down the supply chain so at every level price adjustments need to be made. Trying to buy market share with price drops should be a thing of the past. If everyone makes these adjustments then the sector will be able operate at a sustainable level. In addition, accurate stock levels can then help determine correct installation dates for both domestic and commercial projects. The big question is how long will the price rises continue? There are so many contributing factors, with energy costs being a significant one.